M17_ Patient Patience

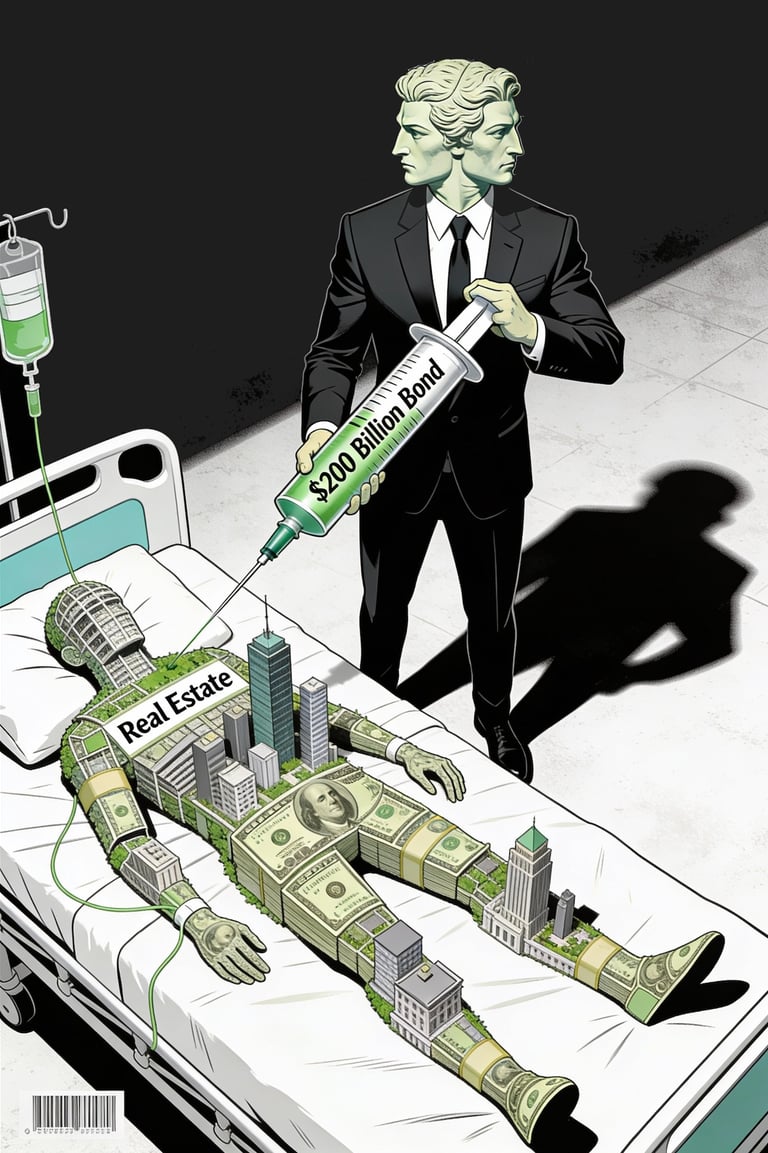

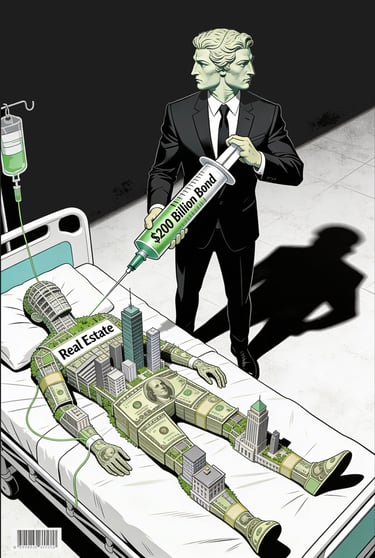

As a follow-up to my January 8th Memo, M16_ Trump's Housing Double Whammy; Bonds and Bans in 2026 NYC, we navigate the final weeks of January—the month of Janus, the two-faced Roman god of thresholds and transitions—the "housing reset" of 2026 has already crossed its first major psychological and financial barrier. Just days after the administration announced its dual-pronged strategy to purchase $200 billion in mortgage bonds and ban large institutional investors from the single-family market, the results are appearing in real-time. On Friday, January 9, mortgage rates dropped to 5.99%, breaking the 6% ceiling for the first time in nearly three years.

Martin O. W. DuPain

1/12/20263 min read

The Success of "Shadow QE"

The first face of this policy—directed at the financial side of the equation—is already proving its effectiveness. Treasury officials have labeled this move "Shadow QE," as it explicitly uses the cash reserves of Fannie Mae and Freddie Mac to offset the Federal Reserve’s ongoing balance sheet reduction. By stepping in as a massive buyer of mortgage-backed securities, the government has successfully compressed risk premiums.

For the average homebuyer, the move from 6.2% to 5.99% is not just a symbolic victory. Analysis shows that for a buyer with a $3,000 monthly budget, this drop translates into roughly $14,000 in additional purchasing power compared to just one month ago. In high-cost markets like New York City, where the homeownership rate is a stagnant 30%, this increased leverage is the first real sign that the rusted hinges of the market are beginning to move.

Cracking the "Housing Lock"

For years, New York City has been trapped in a state of "housing lock." Owners who secured 3% mortgage rates during the pandemic have been essentially frozen in place, unwilling to sell because moving would mean doubling their interest costs.

By forcing market rates toward the 5% handle, the administration is attempting to weaken the "golden handcuffs" that have kept inventory at a seven-year low. In NYC’s unique landscape of condos and co-ops, lower rates provide a glimmer of hope for a long-overdue transition. It offers a way for those stuck in the "Sisyphus" cycle of endless renting to finally move toward ownership as the boulder of high interest rates begins to roll downhill.

The Investor Ban and the Price Paradox

The second face of the policy—the ban on "mega-investors" (those owning 1,000+ homes)—targets the perceived villains of the affordability crisis. While Blackstone and its subsidiaries are the primary targets rather than BlackRock, the direct impact on NYC is statistically small. Institutional "mega-investors" own nearly zero percent of the single-family rental stock in the five boroughs.

However, the real benefit for NYC may be a leveling of the playing field. For the last decade, cash buyers have accounted for roughly 41% of all NYC residential sales, often outcompeting families who rely on mortgage financing. If lower rates make mortgages more affordable and attractive, individual buyers gain a fighting chance against the all-cash entities that have long dominated the threshold of the market.

Will Prices Come Down Soon?

While "Shadow QE" has fixed the finance side of the equation, the supply side remains a different beast. There is a potential price paradox ahead:

* National Inflation: Organizations like the NAR project that national home prices could actually rise by roughly 4% in 2026. This is because lower rates bring millions of qualified buyers back into the market faster than new houses can be built.

* The Supply Gap: We remain millions of units short of demand. Without a massive increase in new construction, making money "cheaper" often just means more people are bidding on the same limited number of homes.

* The Price Floor: The only factor that might push prices down is if the ban on large investors yanks the "price floor" out of regional hubs like Atlanta or Phoenix. While this could cause a price shock in those areas, NYC is largely insulated from this because it never had a high concentration of these institutional single-family owners to begin with.

Conclusion: A New Baseline

The first face of Janus has looked back at the high-rate environment and slammed the door. We are entering a transition where 5.99% is the new baseline.

For NYC and similar markets, the "double whammy" is currently acting as a stabilization tool, not a price-cutting tool. It has successfully improved usability for the average buyer, but until the chronic shortage of new housing is addressed, we are likely to see a market where prices remain firm even as monthly payments become more manageable.

Think of the housing market as an ancient temple with a massive, rusted door. The $200 billion bond purchase is the grease on the hinges that finally allows the door to move. The investor ban removes the giants who were crowding the entrance. The door is now open and the music is quieter, but there is still a massive line of people outside and not enough room for everyone in the temple. The "reset" has begun, but the journey to true affordability still requires building more rooms.

For further discussions, inquiries or to delve deeper into this analysis, please feel free to get in touch.